How the Market Bets on the Fed

Whenever the topic of interest rates and the Federal Reserve comes up, we often hear analysts refer to the market’s expectations of what the rate will be, versus what the Fed says it will be. For example, currently the Fed is not expecting to make any cuts to the rate this year, and say the rate will probably be 5% or more at the end of 2023. But then we hear the market is expecting the Fed to do one cut and the rate will be less than 5 by December.

So, where does that market expectation come from? What mechanism is used to gauge the market expectation of future interest rates?

There’s a big hint there in the word “future,” because the answer is in the futures market. Specifically, a futures contact called the 30 Day Federal Funds (ZQ). This futures contract, offered by the CME, is based on the average Fed Funds rate during the contract month. The price is derived from the interest rate, and there are contacts for up to 60 months in the future.

In case you are not familar with interest rate futures, let’s review how these contracts are priced. The price of contract is interest rate subtracted from 100. So if the expected Fed Funds rate is 7.25%, then the price is 92.75. Conversely, if the futures price is 96.40, then the expected rate would be 3.60%.

This main purpose of this contract (and its associated options) is to allow large investors to hedge short term interest rate risk and other interest rate related strategies. The contract trades on the CME, and although it was not created to be a gauge of market sentiment, it has become a useful way to see how the market feels about future rates.

Let’s take a look at the market and see what it tells us about the future rate. Here is a screen shot of the next year’s worth of the 30 Day Fed Fund contracts. As of right now, the Feburary contact last traded at 95.405. We can calculate the fund rate using 100 - Price, so this equates to an expected averate rate of 4.595% in February. We can do the thing for June and December and see the rate go up to 4.915% and then back down to 4.55%. So the market does appear to be expecting a rate cut before the end of the year.

https://www.cmegroup.com/markets/interest-rates/stirs/30-day-federal-fund.quotes.html

Fortunately for us, we don’t have do those calculations every time we want to check market sentiment. Instead, we can use the CME FedWatch Tool to see more detail into the market expections. For each month ahead the FedWatch tool uses the futures (and perhaps options) to calculate the percenages for likely rates that month.

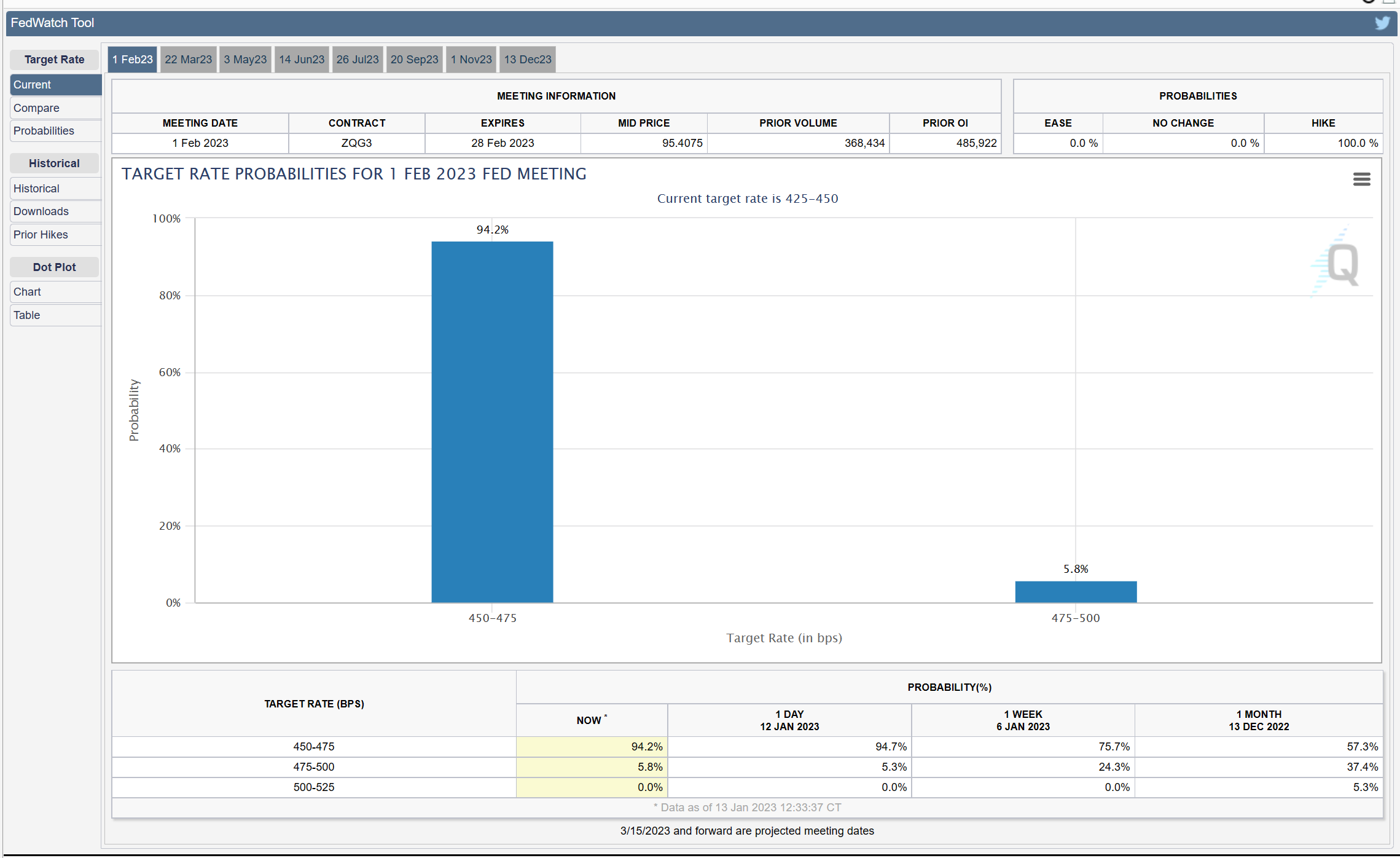

Let’s compare that with the CME’s FedWatch Tool. Currently there is a 94% chance of the rate being between 4.50-4.75 in Feburary, so that is consistent with the futures price that is about 4.6%

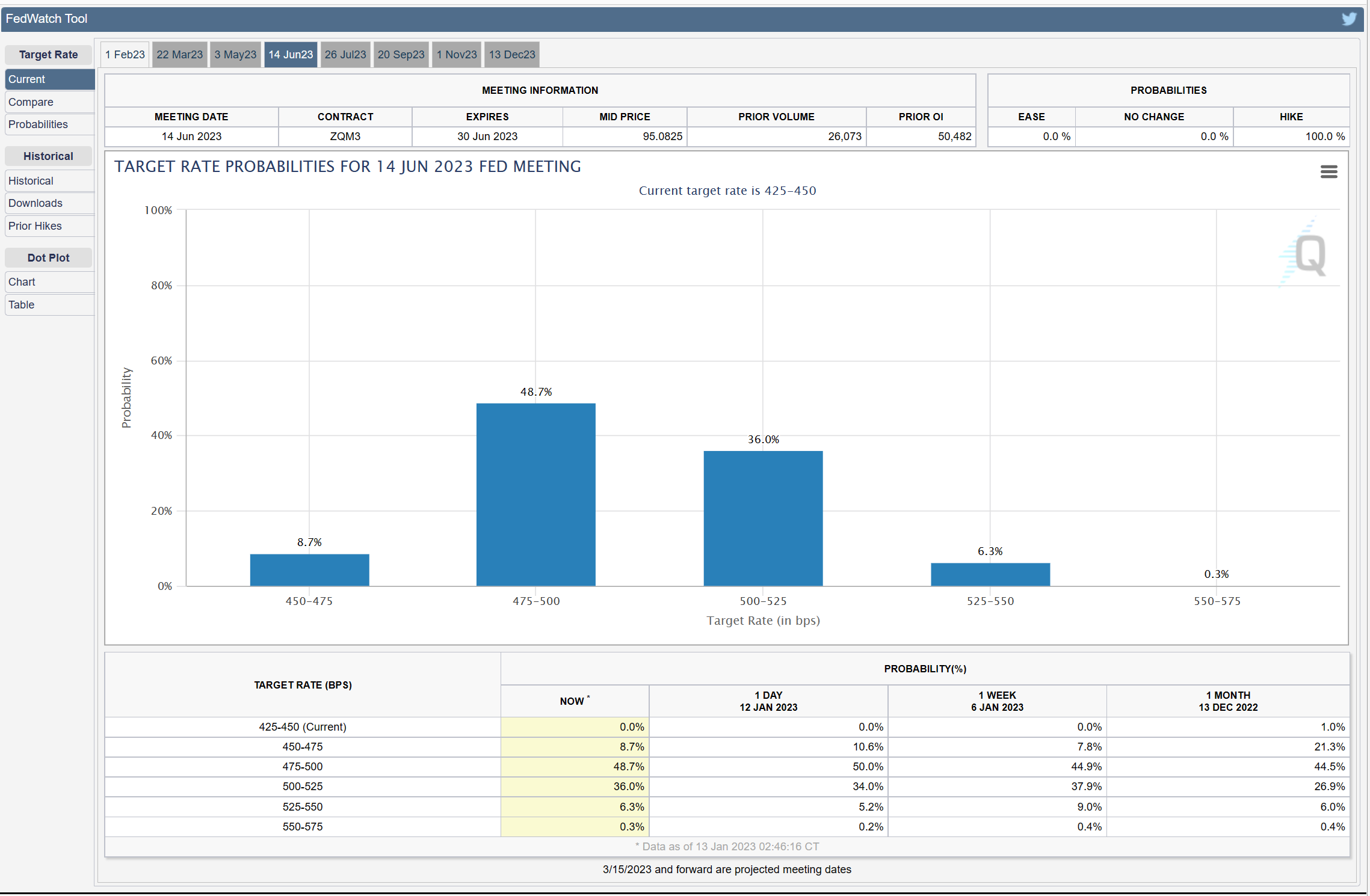

For June, FedWatch says there is a 49% chance the rate will be between 4.75-5.00%, and that is also consistent with the futures price of 4.92%.

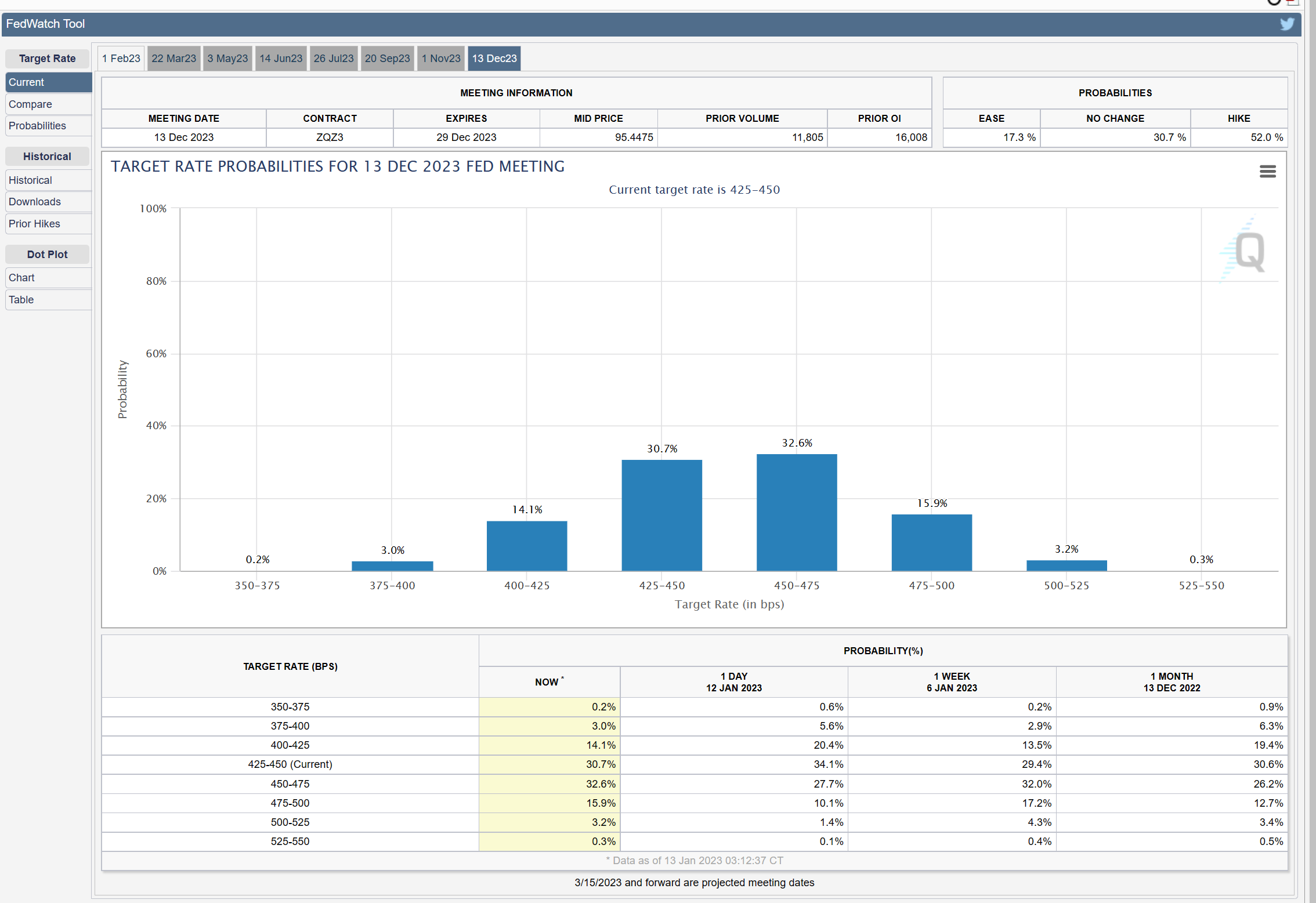

In December FedWatch shows 32.6% (the current highest one of many possibilities) for the 4.50-4.75% range, again consistent with the 4.55% predicted by the futures price.